Signing a medical release after an accident means you have authorized another party – typically an insurance company – to access some or all of your medical records. Whether that signature damages your personal injury case depends heavily on what you signed, when you signed it, and who asked you to sign it.

This guide focuses specifically on what Pennsylvania accident victims need to know after signing a medical release – and whether the damage can be undone.

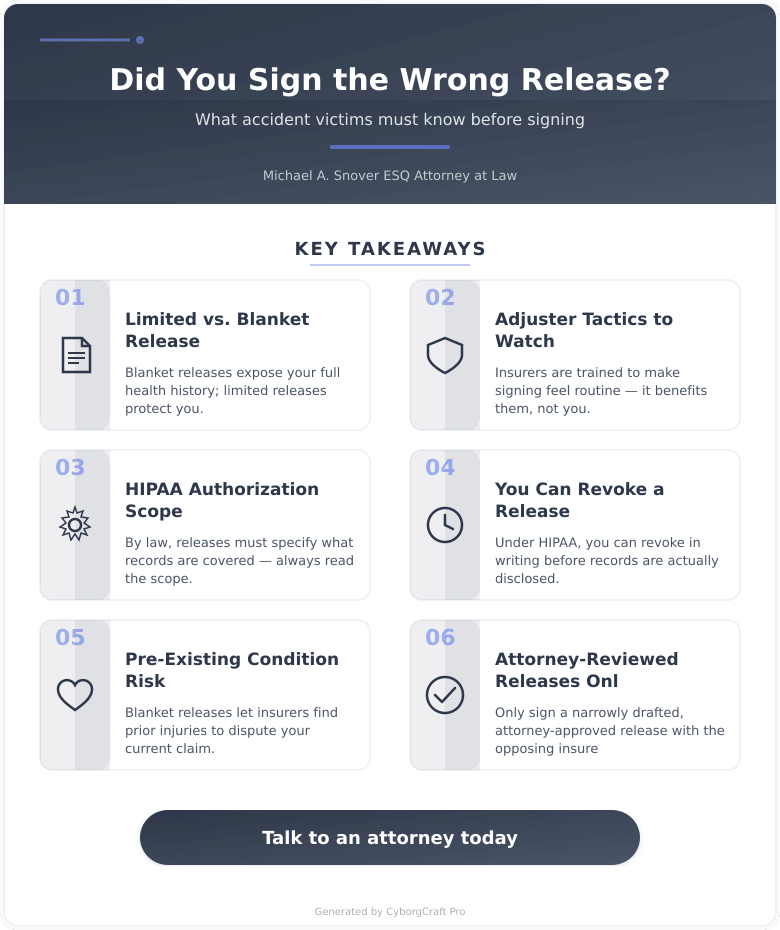

If you signed something and immediately felt a pit in your stomach, you’re not alone. The most common mistake we see is injured people signing documents handed to them by an adjuster within days of a crash – before they’ve spoken with anyone who actually represents their interests. It happens constantly, and it’s not your fault. Adjusters are trained to make these requests feel routine.

What a Medical Release Actually Authorizes

Medical Authorization Definition: A medical release (also called a HIPAA authorization form) is a signed document that grants a named party legal access to your protected health information held by your doctors, hospitals, or insurers.

There are two very different types of releases you could have signed:

- A limited release – covers only records related to the accident injury, specific dates, or named providers

- A blanket release – gives the insurance company access to your entire medical history, including unrelated conditions, prior injuries, and mental health records

According to the U.S. Department of Health and Human Services, HIPAA authorizations must specify the scope of information being released – but many injured people never read that scope before signing.

The difference matters enormously. A blanket release hands insurers ammunition to hunt for pre-existing conditions, prior claims, or anything else they can use to argue your injuries aren’t accident-related.

Signed a Medical Release vs. Not Signing: Which Approach Works?

Where signing a limited release succeeds: It allows your own insurer to coordinate benefits, satisfies legitimate documentation requests, and can move a claim forward faster when the scope is narrow and controlled.

Where signing a limited release fails: Even narrow releases can be misused if the language is vague. Insurers may argue a broad interpretation of “related” records.

Where signing a blanket release succeeds: Rarely benefits the injured person. It may satisfy an adjuster quickly, but that speed benefits the insurer, not you.

Where signing a blanket release fails: It exposes your entire health history. Insurers can use unrelated conditions to dispute causation, reduce settlement offers, or deny claims outright.

The verdict: A limited, attorney-reviewed release is the only type an injured person should ever sign when dealing with the opposing insurer. Blanket releases handed to you by adjusters should be reviewed – and likely rejected – before signing.

| Release Type | Scope | Risk Level | Best For |

|---|---|---|---|

| Limited Release | Accident-related records only | Low to moderate | Coordinating your own insurance |

| Blanket Release | Full medical history | High | Nobody – avoid if possible |

| Attorney-Drafted Release | Narrowly defined, controlled | Lowest | All personal injury situations |

Thinking about this for your situation? Let’s talk. Contact us and we’ll walk you through your options – no pressure, no obligation.

Can You Undo a Medical Release You Already Signed?

Here’s what surprises most people: in many cases, you can revoke a medical authorization. Under HIPAA, a signed release can generally be revoked in writing – but only to the extent the information hasn’t already been disclosed. If the insurer already pulled your records, revocation won’t undo that.

Insurance companies commonly request records promptly after receiving a signed release, which means speed matters here.

If you signed recently and records haven’t been pulled yet, a written revocation sent directly to your medical providers may stop the disclosure. An attorney can help you draft that revocation and notify the right parties fast.

Your Medical Release Action Plan

- Step 1 – Locate the document: Find your copy of what you signed and identify whether it’s a limited or blanket release. Look for provider names, date ranges, and any language like “all records” or “any and all.”

- Step 2 – Note the date: The sooner you act, the better your options.Once a release has been honored, any records already disclosed cannot be unwound — HIPAA revocation only stops future disclosures.

- Step 3 – Contact your medical providers: Notify every named provider in writing that you are considering revoking authorization. Ask whether records have been released yet.

- Step 4 – Speak with an attorney immediately: Before taking any further steps, get legal guidance. An attorney can review the document, assess the damage, and help you control what happens next.

- Step 5 – Stop responding to the adjuster directly: Once you have legal representation, all communication goes through your attorney. Do not sign anything else without review.

What Pennsylvania Law Says About Your Rights

Pennsylvania follows the Pennsylvania bad faith statute (42 Pa.C.S. § 8371) and the Pennsylvania Insurance Department guidelines, which require insurers to act in good faith. Pressuring an injured claimant to sign a broad medical release immediately after an accident – before they’ve had time to understand their rights – can raise bad faith concerns under Pennsylvania law (2026).

Pennsylvania’s statute of limitations for personal injury claims is generally two years from the date of the accident. But time-sensitive document issues like medical releases need attention now, not eventually. Waiting reduces your options.

Serving clients throughout the Lehigh Valley, including Bethlehem, Allentown, Easton, Nazareth, and surrounding Northampton and Lehigh Counties, Michael A. Snover ESQ Attorney at Law understands how quickly these situations can shift against an injured person who acts without guidance.

Preparation Checklist Before Your Attorney Consultation

- ☐ Copy of every document you signed after the accident

- ☐ Name and contact info of the insurance adjuster who requested the release

- ☐ List of all medical providers who treated you after the accident

- ☐ Date you signed the release

- ☐ Any written or email communication from the insurer

- ☐ Accident report and any photos from the scene

Key Takeaways for Pennsylvania Accident Victims in 2026

- A blanket medical release is dangerous – it gives insurers access to your full health history, which they can use to minimize your claim

- Revocation may still be possible – if records haven’t been disclosed yet, written revocation to your providers could stop the damage

- Limited releases are not automatically harmful – scope and timing determine risk, not the act of signing alone

- Pennsylvania law protects you – insurer bad faith in obtaining releases can be challenged under Pennsylvania’s bad faith statute, 42 Pa.C.S. § 8371

- Act fast – the two-year statute of limitations doesn’t help you if records are already compromised early in the process

Frequently Asked Questions

Does signing a medical release automatically hurt my personal injury case?

Not automatically – it depends on the scope of what you signed. A limited release tied to your accident injuries carries far less risk than a blanket release covering your full medical history. The damage, if any, depends on what the insurer has already accessed.

Can an insurance company require me to sign a medical release?

Your own insurer may require limited releases for first-party benefits, but the opposing insurer cannot legally compel you to sign anything. An adjuster asking you to sign is not the same as a legal requirement. Always review what you’re signing before agreeing.

How quickly can an insurer access my records after I sign?

Insurers commonly request records promptly after receiving a signed release. This is why immediate action matters if you’ve already signed and want to explore revocation options.

What is the statute of limitations for personal injury in Pennsylvania?

Pennsylvania generally allows two years from the date of the accident to file a personal injury lawsuit. Missing this deadline typically bars your claim entirely, regardless of the strength of your case.

Should I talk to the insurance adjuster before hiring an attorney?

Talking to the opposing insurer before getting legal advice puts you at a significant disadvantage. Adjusters are trained negotiators working to limit payouts. Anything you say – or sign – can be used to reduce your claim’s value.

How much does a personal injury attorney cost in Pennsylvania?

Most personal injury attorneys in Pennsylvania work on a contingency fee basis, meaning you pay nothing unless you recover compensation. Industry-standard contingency fees typically range from 33% to 40% of the recovery, with the exact percentage varying by firm and case complexity.

Can I revoke a medical release I already signed?

Yes, in most cases you can revoke a HIPAA authorization in writing – but only before records have been disclosed. Once information has been shared, revocation cannot undo that disclosure, which is why acting quickly matters.

About the Author

The Michael A. Snover ESQ Attorney at Law Team, personal injury attorneys in Bethlehem, PA. For more information about our approach, visit our homepage or explore our services. Our office is located at 2571 Baglyos Circle, Suite B25, Bethlehem, PA 18020.

Ready to take the next step? Contact us today for straight answers about your situation. The sooner you act, the more options you have – and a free consultation costs you nothing.